တိုက်ရိုက်အဖြေ: photovoltaic လုပ်ငန်းတွင် ငွေအသုံးပြုမှုသည် ခန့်မှန်းခြေအားဖြင့် 2024 ခုနှစ်တွင် တန်ချိန် 6,146 တန်အထိရောက်ရှိခဲ့သည်။, ၊ အရာသည် ကမ္ဘာလုံးဆိုင်ရာ ငွေလိုအပ်ချက်၏ 17% ကို ကိုယ်စားပြုသည်။. သို့သော် ငွေဈေးနှုန်းများ မြင့်တက်လာခြင်းကြောင့် 2025 ခုနှစ်တွင် 70% ကျော် မြင့်တက်ခဲ့သည်။ ကျော်လွန်ရန် တစ်အောင်စလျှင် $80—ထုတ်လုပ်သူများကို တွန်းအားပေးနေသည်မှာ “ငွေလျှော့ချရေး” နည်းဗျူဟာများ. ၎င်းတို့တွင် ပါဝင်သည်မှာ ငွေရောင်အုပ်ထားသော ကြေးနီအနှစ်များ (ငွေပါဝင်မှုကို 50-80% လျှော့ချခြင်း)၊, ကြေးနီလျှပ်စစ်ဓာတ်ဖြင့် သတ္တုရည်စိမ်နည်းပညာများ, ၊ နှင့် အဆင့်မြင့်ဆဲလ်ပုံစံများကဲ့သို့ TOPCon နှင့် HJT. ထိပ်တန်းထုတ်လုပ်သူများကဲ့သို့ LONGi နှင့် Aiko Solar သည် 2026 ခုနှစ်အစောပိုင်းတွင် ငွေမပါသော module များကို gigawatt-scale ဖြင့် ထုတ်လုပ်နေပြီဖြစ်သည်။.

သော့ထုတ်ယူမှုများ

ငွေသည် ကျောရိုးအဖြစ် ဆက်လက်တည်ရှိနေသည်။ ဆိုလာဆဲလ်လျှပ်ကူးပစ္စည်းထုတ်လုပ်ခြင်း၏ အဓိကအကြောင်းရင်းမှာ ၎င်း၏ လျှပ်စစ်စီးကူးနိုင်စွမ်းနှင့် မည်သည့်အရာနှင့်မျှ မတူသောကြောင့်ဖြစ်သော်လည်း သတ္တု၏ ဈေးနှုန်းအပြောင်းအလဲမြန်ခြင်း သည် photovoltaic ထုတ်လုပ်သူများအတွက် အရေးပါသော ကုန်ကျစရိတ်ဖိအားတစ်ခု ဖြစ်လာခဲ့သည်။ လုပ်ငန်းသည် အသုံးပြုခဲ့သည်။ 197.6 သန်း အောင်စ (ခန့်မှန်းခြေအားဖြင့် တန်ချိန် 6,146 တန်) ငွေကို 2024 ခုနှစ်တွင် အသုံးပြုခဲ့ပြီး၊ ၎င်းသည် ခန့်မှန်းခြေအားဖြင့် ကမ္ဘာလုံးဆိုင်ရာ စက်မှုငွေလိုအပ်ချက်၏ သုံးပုံတစ်ပုံ.

ဈေးနှုန်းများ အဆမတန်မြင့်တက်လာခြင်း—2024 ခုနှစ်အစောပိုင်းတွင် တစ်အောင်စလျှင် အလယ်အလတ် $20 မှ အထွတ်အထိပ်သို့ ရောက်ရှိခဲ့သည်။ 2025 ခုနှစ် ဒီဇင်ဘာလတွင် $84—အစားထိုးရန် ကြိုးပမ်းမှုများကို အရှိန်မြှင့်တင်ခဲ့သည်။. ငွေရောင်အနှစ်သည် ယခုအခါ ဆိုလာဆဲလ်ထုတ်လုပ်မှုကုန်ကျစရိတ်၏ 14-30% ကို ကိုယ်စားပြုသည်။, ၊ 2023 ခုနှစ်တွင် 5% သာရှိရာမှ ထုတ်လုပ်သူများအား ငွေလျှော့ချရေး တီထွင်မှုများကို ဦးစားပေးလုပ်ဆောင်ရန် တွန်းအားပေးနေသည်။.

အဓိကနည်းလမ်းသုံးခု ငွေအပေါ်မှီခိုမှုကို ဖြေရှင်းရန် ပေါ်ပေါက်လာသည်-

- ငွေရောင်အုပ်ထားသော ကြေးနီအနှစ်များ သည် ချက်ချင်းဖြေရှင်းနည်းကို ပေးစွမ်းနိုင်ပြီး၊ ငွေပါဝင်မှုကို 15-30% အထိ လျှော့ချနိုင်ပြီး လက်ရှိစခရင်ပုံနှိပ်ခြင်း အခြေခံအဆောက်အအုံနှင့် တွဲဖက်အသုံးပြုနိုင်စွမ်းကို ထိန်းသိမ်းထားသည်။.

- ကြေးနီလျှပ်စစ်ဓာတ်ဖြင့် သတ္တုရည်စိမ်ခြင်း သည် ပိုမိုပြင်းထန်သောချဉ်းကပ်မှုကို ကိုယ်စားပြုပြီး၊ semiconductor အဆင့် သတ္တုရည်စိမ်နည်းပညာများမှတစ်ဆင့် ငွေကို လုံးဝဖယ်ရှားပေးသော်လည်း ထုတ်လုပ်မှုလိုင်းအသစ်များတွင် သိသာထင်ရှားသော ရင်းနှီးမြှုပ်နှံမှုများ လိုအပ်ပါသည်။.

- အကောင်းဆုံးဆဲလ်ပုံစံများ—အထူးသဖြင့် heterojunction (HJT) နှင့် back-contact (BC) ဒီဇိုင်းများသည် ကြေးနီပေါင်းစပ်မှုကို အထောက်အကူဖြစ်စေပြီး အလုံးစုံစွမ်းဆောင်ရည်ကို မြှင့်တင်ပေးသည့် အပူချိန်နိမ့်သော လုပ်ဆောင်ခြင်းကို လုပ်ဆောင်နိုင်သည်။.

အဓိကထုတ်လုပ်သူများသည် ကြီးမားသောစကေးဖြင့် စတင်အသုံးပြုနေပြီဖြစ်သည်။. LONGi Green Energy သည် 2026 ခုနှစ် Q2 တွင် ကြေးနီသတ္တုပါဝင်သော back-contact ဆဲလ်များကို အမြောက်အမြားထုတ်လုပ်ရန် အစီအစဉ်များကို အတည်ပြုခဲ့ပြီး၊ Aiko Solar တိုးချဲ့ခဲ့သည်။ 10 gigawatts ငွေမပါသော “ABC” module များဖြစ်သည်။ စက်မှုလုပ်ငန်းဆိုင်ရာ လေ့လာသုံးသပ်သူများက ကြေးနီသတ္တုရည်စိမ်ခြင်းသည် 2030 ခုနှစ်တွင် 50% ဈေးကွက်ဝေစုကို ရရှိပါက၊, ဆိုလာမှ ငွေလိုအပ်ချက်သည် တစ်နှစ်လျှင် အောင်စ ၂၆၀ သန်းအထိ လျော့ကျသွားနိုင်သည်။.

အဘယ်ကြောင့် ငွေသည် Photovoltaic ထုတ်လုပ်မှုကို လွှမ်းမိုးထားသနည်း။

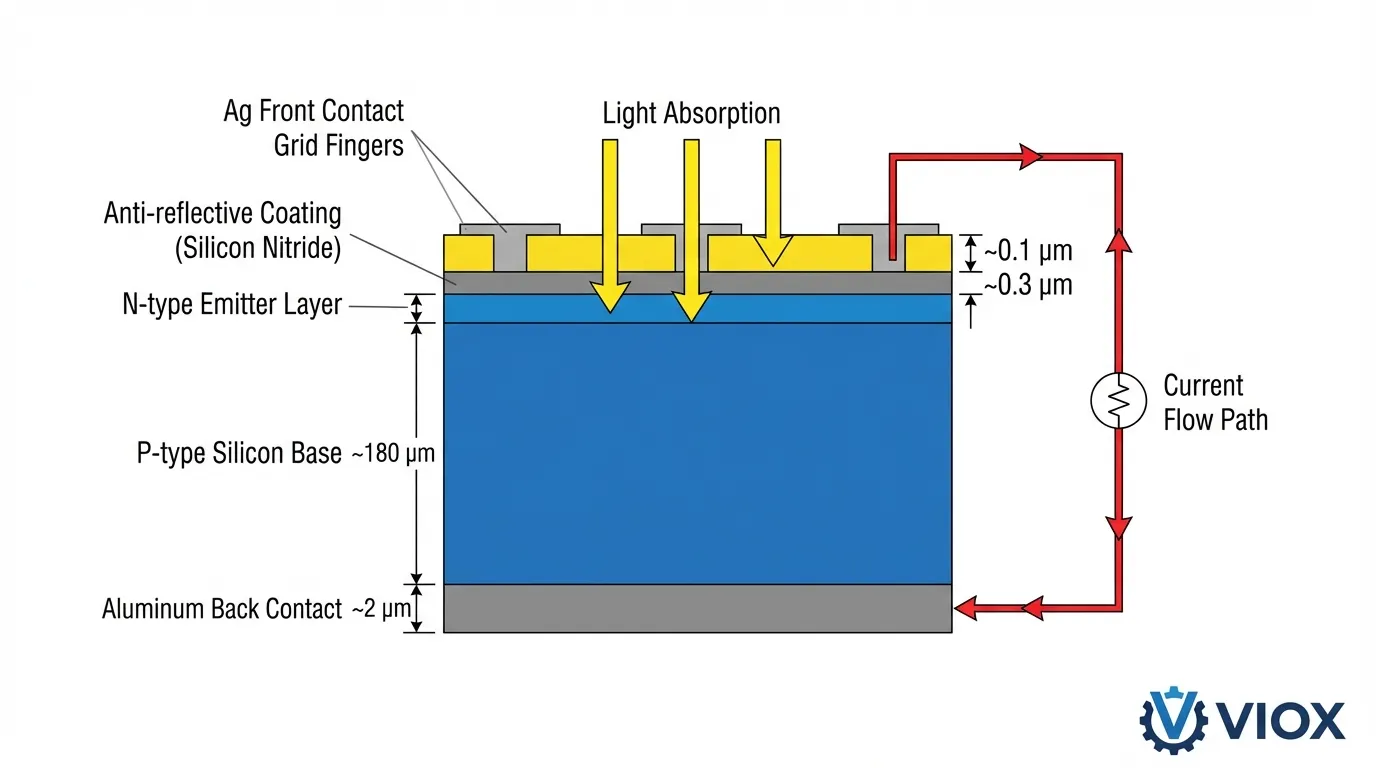

ဆိုလာဆဲလ်ထုတ်လုပ်ရာတွင် ငွေ၏အခန်းကဏ္ဍသည် အခြားရွေးချယ်စရာပစ္စည်းများနှင့် မတူညီသော ရုပ်ပိုင်းဆိုင်ရာဂုဏ်သတ္တိများ၏ ထူးခြားသောပေါင်းစပ်မှုမှ ပေါက်ဖွားလာခြင်းဖြစ်သည်။ နှင့်အတူ သတ္တုအားလုံး၏ လျှပ်စစ်စီးကူးနိုင်စွမ်း အမြင့်ဆုံး (20°C တွင် 63.0 × 10⁶ S/m)၊ ငွေသည် အနည်းဆုံးခံနိုင်ရည်ရှိသော ဆုံးရှုံးမှုများနှင့်အတူ ဆိုလာဆဲလ်မျက်နှာပြင်တစ်လျှောက်တွင် ထိရောက်သော အီလက်ထရွန်စုဆောင်းခြင်းနှင့် သယ်ယူပို့ဆောင်ခြင်းကို လုပ်ဆောင်နိုင်သည်။.

ဟိ သတ္တုရည်စိမ်ခြင်းလုပ်ငန်းစဉ် crystalline silicon ဆိုလာဆဲလ်များအတွက် အားကိုးသည်။ ငွေရောင်အနှစ်—အလွန်ကောင်းမွန်သော ငွေမှုန်များ (ပုံမှန်အားဖြင့် ၀.၅-၂ မိုက်ခရိုမီတာ)၊ ဖန်မှုန်နှင့် အော်ဂဲနစ်ချည်နှောင်ပစ္စည်းများပါဝင်သော ပေါင်းစပ်ပစ္စည်းတစ်ခုဖြစ်သည်။ အတွင်း အပူချိန်မြင့်မားသော မီးဖုတ်ခြင်းလုပ်ငန်းစဉ် (ရိုးရာဆဲလ်များအတွက် 700-900°C)၊ ဖန်မှုန်သည် ရောင်ပြန်ဟန့်တားနိုင်သော ဆီလီကွန်နိုက်ထရိုက်အလွှာမှတဆင့် ထွင်းထုထားပြီး ငွေမှုန်များသည် ဆီလီကွန်အလွှာနှင့် တိုက်ရိုက် ohmic ထိတွေ့မှုကို ပြုလုပ်နိုင်သည်။ ဒါက “မီးလောင်ကျွမ်းနိုင်စွမ်း” 1 mΩ·cm² အောက်ရှိ contact resistances ကိုရရှိစဉ်တွင် ကုန်ကျစရိတ်သက်သာသော screen-printing ထုတ်လုပ်မှုကို လုပ်ဆောင်နိုင်သည်။.

conductivity အပြင်၊ ငွေ၏ optical ဂုဏ်သတ္တိများ panel တစ်ခုလုံး၏ စွမ်းဆောင်ရည်ကို အထောက်အကူပြုသည်။ သတ္တု၏ high reflectivity (ဆိုလာရောင်ခြည်တစ်လျှောက် >95%) သည် ရှေ့ဘက်ရှိ grid fingers များတွင် အလင်းဝင်ရောက်မှုကို လျှော့ချပေးပြီး photons များကို active silicon အလွှာထဲသို့ ပိုမိုညွှန်ကြားပေးသည်။ ငွေ၏ oxidation နှင့် corrosion ကိုခံနိုင်ရည် သည် ပြင်ပပတ်ဝန်းကျင်တွင် ရေရှည်တည်ငြိမ်မှုကို သေချာစေပြီး စက်မှုလုပ်ငန်း၏ ၂၅-၃၀ နှစ် အာမခံစံနှုန်းများကို ထောက်ပံ့ပေးသည်။.

Cell နည်းပညာဖြင့် ငွေသုံးစွဲမှု

photovoltaic စက်မှုလုပ်ငန်း၏ ငွေအသုံးပြုမှုသည် နည်းပညာအကူးအပြောင်းများနှင့်အတူ သိသိသာသာ ပြောင်းလဲလာခဲ့သည်-

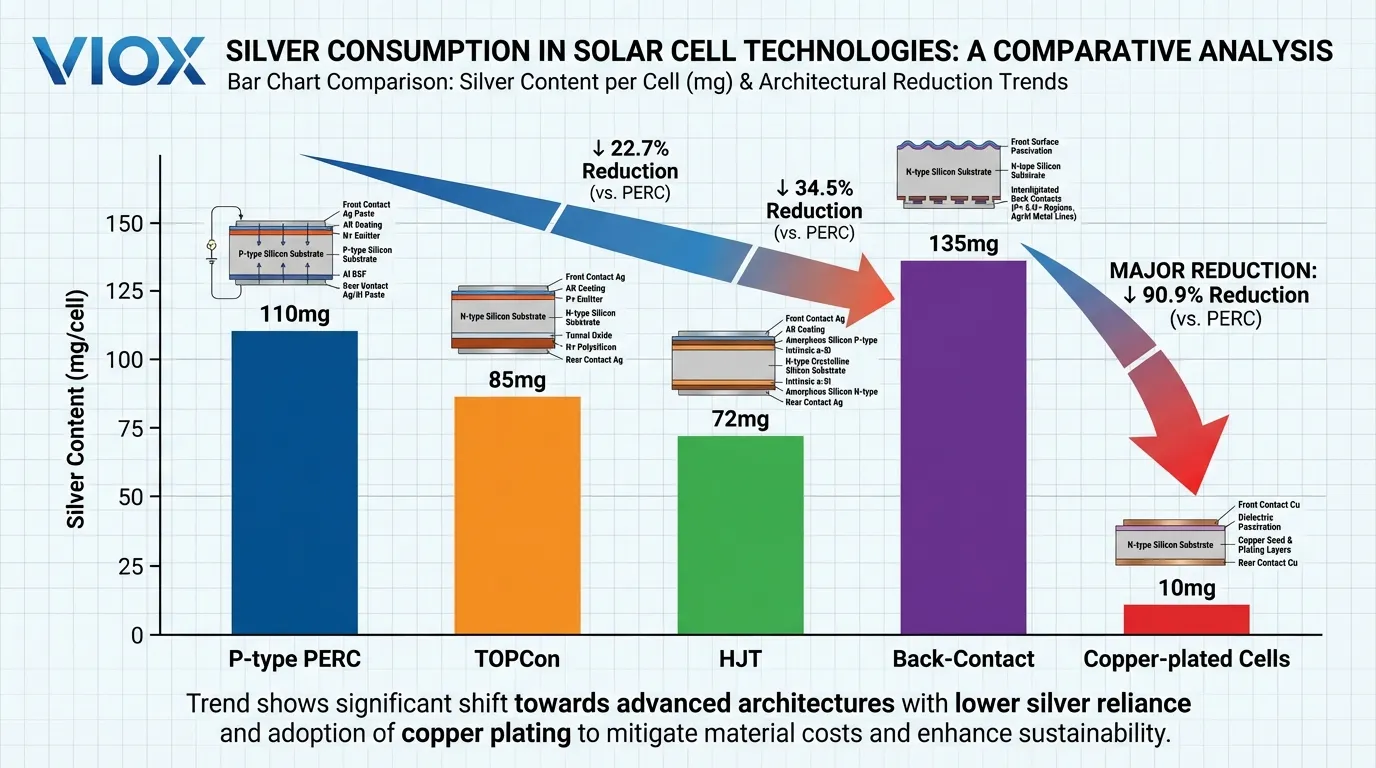

- P-type PERC နည်းပညာ- ဆဲလ်တစ်ခုလျှင် ငွေ ၁၀၀-၁၁၀ မီလီဂရမ်ခန့်

- TOPCon ဆဲလ်များ- ဆဲလ်တစ်ခုလျှင် ၈၀-၉၀ မီလီဂရမ်

- Heterojunction (HJT) ဒီဇိုင်းများ- ၇၀-၇၅ မီလီဂရမ်

- Back-contact (BC) ဆဲလ်များ- ၁၃၅ မီလီဂရမ်အထိ

ဤကိန်းဂဏန်းများသည် စောပိုင်းထပ်တလဲလဲများမှ လျှော့ချမှုများကို ကိုယ်စားပြုသော်လည်း၊ ကမ္ဘာလုံးဆိုင်ရာ ထုတ်လုပ်မှုပမာဏကို ကျော်လွန်၍ မြှောက်သောအခါတွင် အကြွင်းမဲ့သုံးစွဲမှုသည် များပြားနေဆဲဖြစ်သည်။ နှစ်စဉ် ဆဲလ်ထုတ်လုပ်နိုင်စွမ်း 700 gigawatts.

ထောက်ပံ့မှု အားနည်းချက်

ဆိုလာကဏ္ဍ၏ ငွေအပေါ်မှီခိုမှုသည် structural အားနည်းချက်. ကို ဖန်တီးသည်။ ကြေးနီ သို့မဟုတ် အလူမီနီယမ်နှင့်မတူဘဲ၊ ခန့်မှန်းခြေအားဖြင့် ငွေထုတ်လုပ်မှု၏ 70% သည် ဘေးထွက်ပစ္စည်းအဖြစ် ဖြစ်ပေါ်သည်။ ခဲ၊ သွပ်နှင့် ကြေးနီသတ္တုတူးဖော်ခြင်း။ ဆိုလိုသည်မှာ ငွေထောက်ပံ့မှုတိုးတက်မှုသည် အခြားသတ္တုဈေးကွက်များ၏ စီးပွားရေးအပေါ် ကန့်သတ်ထားပြီး photovoltaic လိုအပ်ချက်ကို တုံ့ပြန်ရာတွင် စက်မှုလုပ်ငန်း၏ ထုတ်လုပ်မှုကို တိုးချဲ့နိုင်စွမ်းကို ကန့်သတ်ထားသည်။.

မူလငွေသတ္တုတွင်းထွက်ရှိမှုသည် ခန့်မှန်းခြေအားဖြင့် တန့်နေခဲ့သည်။ နှစ်စဉ် အောင်စ ၈၁၃ သန်း, စုစုပေါင်း ငွေလိုအပ်ချက်သည် ရောက်ရှိခဲ့သည်။ ၂၀၂၄ ခုနှစ်တွင် အောင်စ ၁.၁၆ ဘီလီယံ, ဖန်တီးခြင်း၊ ဆက်တိုက် ထောက်ပံ့မှု လိုအပ်ချက်များ ယခုအခါ ငါးနှစ်ဆက်တိုက် တိုးချဲ့ခဲ့သည်။.

ငွေဈေးကွက် အကျပ်အတည်းနှင့် ဆိုလာစီးပွားရေးအပေါ် သက်ရောက်မှု

ငွေဈေးကွက်သည် မကြုံစဖူး ပြောင်းလဲမှု ၂၀၂၄-၂၀၂၅ ခုနှစ်တစ်လျှောက်လုံး photovoltaic ထုတ်လုပ်မှု၏ ကုန်ကျစရိတ်ဖွဲ့စည်းပုံကို အခြေခံအားဖြင့် ပြောင်းလဲခဲ့သည်။ နှစ်ပေါင်းများစွာ အောင်စတစ်စောင်လျှင် $20-25 ဖြင့် အတော်အတန် တည်ငြိမ်သော ဈေးနှုန်းဖြင့် ရောင်းဝယ်ပြီးနောက် ၂၀၂၄ ခုနှစ် အလယ်ပိုင်းတွင် ငွေဈေးနှုန်းများ စတင်မြင့်တက်လာခဲ့သည်။ ၂၀၂၅ ခုနှစ် ဒီဇင်ဘာလတွင် spot ဈေးနှုန်းများသည် ကျော်လွန်သွားခဲ့သည်။ အောင်စတစ်စောင်လျှင် $84- တစ်ခု 170% တိုးလာခြင်း ရွှေ၏ ၇၃% တိုးလာမှုကိုပင် ကျော်လွန်သွားခဲ့သည်။.

ထုတ်လုပ်သူများအပေါ် ကုန်ကျစရိတ် ဖိအား

ဤဈေးနှုန်းပေါက်ကွဲမှုသည် ဆိုလာထောက်ပံ့ရေးကွင်းဆက်တစ်လျှောက် ချက်ချင်းကုန်ကျစရိတ်ဖိအားများကို ဖန်တီးခဲ့သည်။. ငွေ paste, ရုံသာကိုယ်စားပြုသော ၂၀၂၃ ခုနှစ်တွင် စုစုပေါင်း ဆဲလ်ထုတ်လုပ်မှုကုန်ကျစရိတ်၏ 5%, ဖောင်းပွသွားသည်။ ၂၀၂၅ ခုနှစ်နှောင်းပိုင်းတွင် ၁၄-၃၀%, ဆဲလ်နည်းပညာနှင့် paste ဖော်မြူလာပေါ်မူတည်၍။.

TOPCon ဆဲလ်ထုတ်လုပ်သူများအတွက် သက်ရောက်မှုသည် အထူးပြင်းထန်သည်- ဆဲလ်ဈေးနှုန်းများသည် ၂၀၂၅ ခုနှစ် ဒီဇင်ဘာလအနိမ့်ဆုံးမှ ခန့်မှန်းခြေအားဖြင့် ၃၀% တိုးလာသော်လည်း ၎င်းသည် ငွေကုန်ကျစရိတ်ဖောင်းပွမှုနှင့်အတူ လိုက်ပါသွားခဲ့သည်။ Module ထုတ်လုပ်သူများသည် ပိုမိုတင်းကျပ်သော အမြတ်အစွန်းများနှင့် ရင်ဆိုင်ခဲ့ရပြီး၊ ပြင်းထန်သော အမြတ်အစွန်းကျုံ့ခြင်း စက်မှုလုပ်ငန်းတစ်လျှောက် အမြတ်အစွန်းကို ခြိမ်းခြောက်ခဲ့သည်။.

Structural လိုအပ်ချက် အချက်များ

စက်မှုထုတ်လုပ်မှု လိုအပ်ချက်သည် စံချိန်တင် ရောက်ရှိခဲ့သည်။ ၂၀၂၄ ခုနှစ်တွင် အောင်စ ၆၈၀.၅ သန်း, photovoltaics တစ်ခုတည်းက သုံးစွဲခဲ့သည်။ 197.6 သန်း အောင်စ-နီးပါး စက်မှုအသုံးပြုမှု၏ ၂၉%. ။ ကဏ္ဍတစ်ခုတည်းတွင် လိုအပ်ချက်များ စုစည်းခြင်းသည် ဈေးနှုန်း inelasticity, ဆိုလာထုတ်လုပ်သူများသည် ထုတ်လုပ်မှုပမာဏကို စတေးမခံဘဲ သုံးစွဲမှုကို လွယ်ကူစွာ လျှော့ချနိုင်ခြင်းမရှိသောကြောင့်ဖြစ်သည်။.

တစ်ချိန်တည်းမှာပင် ကမ္ဘာလုံးဆိုင်ရာ ဆိုလာတပ်ဆင်မှုပန်းတိုင်များသည် ဆက်လက်အရှိန်မြှင့်နေပြီး၊ အပြည်ပြည်ဆိုင်ရာ စွမ်းအင်အေဂျင်စီသည် 4,000 gigawatts ကို ခန့်မှန်းထားသည်။ of new capacity additions through 2030, potentially pushing solar’s share of total silver demand above 20%.

Supply Constraints

Supply-side constraints compound these demand pressures:

New silver mining projects require 5-8 years from discovery to production, making it impossible for primary supply to respond quickly to price signals. The byproduct nature of most silver production means output is governed by copper, lead, and zinc market cycles rather than silver prices directly.

Geopolitical factors have further tightened physical markets, with တရုတ်နိုင်ငံ—which accounts for approximately 70% of global solar manufacturing capacity—implementing export restrictions on refined silver in 2025, exacerbating liquidity challenges and triggering sharp price volatility.

The Strategic Imperative

For solar manufacturers operating on historically thin margins (typically 5-15% for module producers), the silver cost surge represents an existential threat. A $10 per ounce increase in silver prices translates to approximately $0.02-0.03 per watt in additional cell costs, which can eliminate profitability entirely in competitive markets where module prices have fallen below $0.15 per watt.

This economic pressure has created a clear strategic imperative: manufacturers must either pass costs to customers (risking market share loss), accept compressed margins (threatening long-term viability), or fundamentally redesign their metallization processes to reduce or eliminate silver dependency.

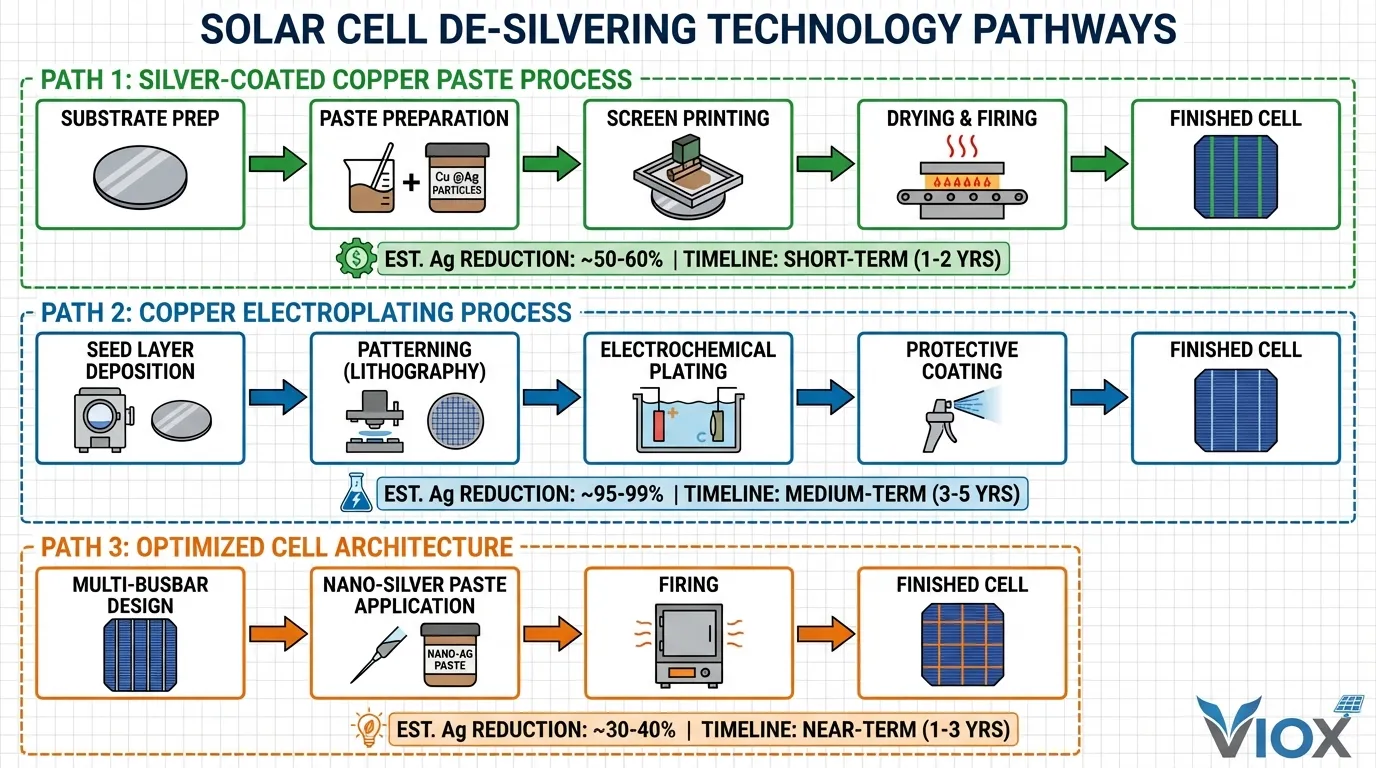

De-Silvering Technologies: From Incremental Thrifting to Complete Substitution

The solar industry’s response to silver price pressures encompasses three distinct technological pathways, each offering different trade-offs between implementation speed, capital requirements, and silver reduction potential.

Silver-Coated Copper Paste: The Immediate Solution

Silver-coated copper (Cu @Ag) paste represents the most rapidly deployable de-silvering technology, offering 50-80% silver reduction while maintaining compatibility with existing screen-printing infrastructure. In this approach, copper particles are coated with a thin silver shell (typically 15-30% silver by weight), creating a composite material that leverages copper’s lower cost while preserving silver’s superior surface properties.

Technical Challenge: The technical challenge lies in preventing copper oxidation during the high-temperature firing process required for contact formation. At temperatures above 700°C, copper readily oxidizes, forming copper oxide layers that dramatically increase contact resistance and reduce cell efficiency. The silver coating acts as a protective barrier, but maintaining shell integrity under thermal stress requires precise control.

HJT Cell Application: For heterojunction (HJT) cells, which process at lower temperatures (180-250°C), silver-coated copper paste has achieved particularly strong adoption. The reduced thermal stress minimizes silver shell degradation and copper diffusion risks, allowing silver content to be reduced to 15-20% while maintaining efficiency comparable to pure silver pastes.

TOPCon Cell Application: TOPCon cells present greater challenges due to their higher firing temperatures (typically 700-850°C). Manufacturers have developed “dual-layer” paste architectures: a thin silver seed layer is first printed and fired to establish ohmic contact and create a copper diffusion barrier, followed by a thick Cu @Ag layer that provides bulk conductivity. This approach enables silver consumption reduction exceeding 50%.

Economic Case: With silver at $80 per ounce and copper at $4 per pound, a 70% reduction in silver content translates to approximately $0.015-0.020 per watt in material cost savings—sufficient to restore profitability for many manufacturers. Capital requirements are minimal, as existing screen-printing lines require only paste formulation changes and minor firing profile adjustments. Cu @Ag paste adoption is projected to reach 30-40% of global cell production by 2027.

Copper Electroplating: The Radical Transformation

ကြေးနီလျှပ်စစ်ဓာတ်ဖြင့် သတ္တုရည်စိမ်ခြင်း represents a fundamentally different approach that eliminates silver entirely by borrowing semiconductor fabrication techniques. Instead of printing and firing metal paste, this method deposits copper through electrochemical processes, achieving fine-line metallization with superior conductivity and mechanical properties.

Process Overview: The process begins with deposition of a thin seed layer (ပုံမှန်အားဖြင့် ကြေးနီ သို့မဟုတ် နီကယ်၊ အထူ 50-200 နာနိုမီတာ) ကို ရုပ်ပိုင်းဆိုင်ရာ အငွေ့ပျံခြင်း (PVD) သို့မဟုတ် sputtering မှတဆင့် ပြုလုပ်သည်။ ထို့နောက် ဤအစေ့အလွှာကို photolithography သို့မဟုတ် လေဆာဖြင့် ဖယ်ရှားခြင်းကို အသုံးပြု၍ ဇယားကွက်ပုံသဏ္ဍာန်ကို သတ်မှတ်သည်။ ပုံဖော်ထားသော အလွှာကို ကြေးနီအိုင်းယွန်းများပါဝင်သော လျှပ်လိုက်ရည်ထဲသို့ နှစ်မြှုပ်ထားပြီး၊ လျှပ်စီးကြောင်းကို အသုံးပြု၍ ကြေးနီကို အစေ့အလွှာပေါ်တွင် ရွေးချယ်၍ စုပုံစေပြီး၊ ဇယားကွက်ကို လိုချင်သောအမြင့် (ပုံမှန်အားဖြင့် 15-30 မိုက်ခရိုမီတာ) အထိ တည်ဆောက်သည်။.

နည်းပညာဆိုင်ရာ အားသာချက်များလျှပ်စစ်ဖြင့် သတ္တုချထားသော ကြေးနီလက်ချောင်းများကို ပြုလုပ်နိုင်သည်။ ပိုကျဉ်းသည်။ (စခရင်ပုံနှိပ်ထားသော အနှစ်အတွက် 40-60 မိုက်ခရိုမီတာနှင့် နှိုင်းယှဉ်ပါက 20-30 မိုက်ခရိုမီတာအထိ) ပိုမိုမြင့်မားသော အချိုးအစားများဖြင့် အရိပ်ဆုံးရှုံးမှုကို လျှော့ချနိုင်ပြီး စီးရီးခုခံမှုကို နိမ့်စေသည်။ သန့်စင်သော ကြေးနီဖွဲ့စည်းပုံသည် ပြသသည်။ 1.7 μΩ·cm ၏ အစုလိုက်အပြုံလိုက် ခံနိုင်ရည်ခန့်မှန်းခြေအားဖြင့် မီးဖုတ်ထားသော ငွေအနှစ်ထက် 40% လျော့နည်းသည်။—ထိရောက်မှု အပြစ်ပေးခြင်းမရှိဘဲ လက်ချောင်းများကို ပိုရှည်စေပြီး ဆဲလ်ပုံစံများကို ပိုကြီးစေသည်။.

စိန်ခေါ်မှုများသို့သော် လျှပ်စစ်ဖြင့် သတ္တုချခြင်းသည် သိသာထင်ရှားသော ရှုပ်ထွေးမှုနှင့် ကုန်ကျစရိတ်ကို မိတ်ဆက်ပေးသည်။ အရင်းအနှီးမြှုပ်နှံမှု ပြီးပြည့်စုံသော သတ္တုချလိုင်းအတွက် အကွာအဝေးမှ တစ်ဂစ်ဂါဝပ်လျှင် ၁၅-၂၅ သန်း—စခရင်ပုံနှိပ်စက်ပစ္စည်းထက် ၃-၄ ဆခန့် မြင့်မားသည်။ အစေ့အလွှာ ညီညာမှု၊ သတ္တုချစီးကြောင်း သိပ်သည်းဆ သို့မဟုတ် လျှပ်လိုက်ရည်ပါဝင်မှုတို့တွင် ကွဲပြားမှုများသည် အထွက်နှုန်းကို လျှော့ချနိုင်သည့် ချို့ယွင်းချက်များကို ဖြစ်စေနိုင်သောကြောင့် လုပ်ငန်းစဉ်ထိန်းချုပ်မှု လိုအပ်ချက်များသည် တင်းကျပ်သည်။.

“ကြေးနီအဆိပ်သင့်ခြင်း” ပြဿနာအပူချိန်မြင့်မားသောအခါ ကြေးနီအက်တမ်များသည် ဆီလီကွန်ထဲသို့ အလွယ်တကူ ပျံ့နှံ့သွားပြီး ပြန်လည်ပေါင်းစည်းရေးစင်တာများအဖြစ် လုပ်ဆောင်ကာ ဆဲလ်ထိရောက်မှုကို ဆိုးရွားစွာ လျှော့ချပေးသည့် နက်ရှိုင်းသောအဆင့် ချို့ယွင်းချက်များကို ဖန်တီးပေးသည်။ ခေတ်မီကြေးနီ သတ္တုချခြင်းကို ဖွင့်ပေးသည့် တိုးတက်မှုသည် အဆင့်မြင့်ဆဲလ် ဗိသုကာလက်ရာများ—အထူးသဖြင့် heterojunction (HJT) နှင့် နောက်ကျောအဆက်အသွယ် (BC) ဒီဇိုင်းများ—ထိရောက်သော လုပ်ဆောင်ချက်များအဖြစ် ပွင့်လင်းမြင်သာသော လျှပ်ကူးပစ္စည်းအောက်ဆိုဒ် (TCO) အလွှာများ သို့မဟုတ် အထူးပြု passivation stacks များကို ထည့်သွင်းထားသည်။ ကြေးနီပျံ့နှံ့မှု အတားအဆီးများ.

စီးပွားဖြစ် ဖြန့်ကျက်ခြင်းထိပ်တန်းထုတ်လုပ်သူများသည် စီးပွားဖြစ် ကြေးနီလျှပ်စစ်ဖြင့် သတ္တုချခြင်း၏ ဖြစ်နိုင်ခြေကို အတိုင်းအတာတစ်ခုအထိ သရုပ်ပြခဲ့ကြသည်။. Aiko Solar ၏ “ABC” (All-Back-Contact) မော်ဂျူးများသည် ကြေးနီသတ္တုချခြင်းကို သီးသန့်အသုံးပြုထားပြီး၊ ရောက်ရှိခဲ့သည်။ စုစုပေါင်း ထုတ်လုပ်မှုစွမ်းရည် ၁၀ ဂစ်ဂါဝပ်. LONGi Green Energy ကြေးနီဖြင့် သတ္တုချထားသော နောက်ကျောအဆက်အသွယ်ဆဲလ်များကို အစုလိုက်အပြုံလိုက် ထုတ်လုပ်ရန် အစီအစဉ်များကို ကြေညာခဲ့သည်။ ၂၀၂၆ ခုနှစ် Q2, ထိရောက်မှုပန်းတိုင်များသည် 26% ကျော်လွန်သည်။.

အကောင်းဆုံး ဆဲလ် ဗိသုကာလက်ရာများနှင့် လုပ်ငန်းစဉ် တီထွင်ဆန်းသစ်မှုများ

တိုက်ရိုက်ပစ္စည်း အစားထိုးခြင်းထက် ကျော်လွန်၍၊, ဆဲလ်ဒီဇိုင်း တီထွင်ဆန်းသစ်မှုများ လက်ရှိစုဆောင်းမှု ထိရောက်မှုနှင့် အကောင်းဆုံး သတ္တုပါဝင်မှုပုံစံများမှတစ်ဆင့် ငွေပြင်းအားကို လျှော့ချပေးသည်။.

Multi-Busbar (MBB) နှင့် Zero-Busbar ဒီဇိုင်းများ၎င်းတို့သည် ရိုးရာ 3-5 busbar အပြင်အဆင်များကို ပါးလွှာသော busbar 9-16 ခုဖြင့် အစားထိုးခြင်း သို့မဟုတ် ဝါယာကြိုးအခြေခံ အပြန်အလှန်ချိတ်ဆက်မှုကို နှစ်သက်သော busbar များကို လုံးဝဖယ်ရှားပေးသည်။ ဤချဉ်းကပ်မှုများသည် လက်ရှိစုဆောင်းမှုကို ပိုမိုညီညာစွာ ဖြန့်ဝေပေးပြီး လက်ချောင်းအကွာအဝေးကို တိုးမြှင့်နိုင်စေသည် (စုစုပေါင်းလက်ချောင်းအရှည်ကို လျှော့ချပေးသည်) စီးရီးခုခံမှုကို နိမ့်စေသည်။ ရလဒ်မှာ စုစုပေါင်း သတ္တုပါဝင်မှုဧရိယာနှင့် သက်ဆိုင်ရာ ငွေသုံးစွဲမှုတွင် ၁၀-၂၀% လျှော့ချခြင်း စုစုပေါင်း သတ္တုပါဝင်မှုဧရိယာနှင့် သက်ဆိုင်ရာ ငွေသုံးစွဲမှုတွင် ၁၀-၂၀% လျှော့ချခြင်း.

နာနို-ငွေ အနှစ်များအချင်း 100 နာနိုမီတာအောက်ရှိ အမှုန်များကို အသုံးပြု၍ အဆင့်မြင့်အနှစ်ဖော်မြူလာများသည် ပိုမိုကောင်းမွန်သော ထုပ်ပိုးသိပ်သည်းဆနှင့် အပူချိန်နိမ့်သော မီးဖုတ်ခြင်းကို ရရှိစေပြီး လျှပ်ကူးနိုင်စွမ်းကို မစတေးဘဲ ပါးလွှာသော ပုံနှိပ်အလွှာများကို ဖွင့်ပေးသည်။ ထုတ်လုပ်သူအချို့သည် ငွေတင်ခြင်းကို အောက်သို့ လျှော့ချထားသည်။ တစ်ဝပ်လျှင် ၁၄ မီလီဂရမ် အကောင်းဆုံး ဖန်သားပြင်ဖွဲ့စည်းမှုများနှင့် ပေါင်းစပ်ထားသော နာနို-ငွေကို အသုံးပြု၍.

ဈေးကွက် လှုပ်ရှားမှုများနှင့် စက်မှုလုပ်ငန်း အသွင်ကူးပြောင်းမှု

de-silvering အကူးအပြောင်းသည် ဆိုလာတန်ဖိုးကွင်းဆက်တစ်လျှောက် ယှဉ်ပြိုင်မှုဆိုင်ရာ လှုပ်ရှားမှုများကို ပြန်လည်ပုံဖော်ခြင်း နည်းပညာဆိုင်ရာ ရပ်တည်မှုနှင့် အရင်းအနှီးရရှိနိုင်မှုအပေါ် အခြေခံ၍ အနိုင်ရသူများနှင့် ရှုံးနိမ့်သူများကို ဖန်တီးပေးသည်။ ကြေးနီအခြေခံ သတ္တုပါဝင်မှုကို အောင်မြင်စွာ အသုံးချနိုင်သော ထုတ်လုပ်သူများသည် သိသာထင်ရှားသော ကုန်ကျစရိတ် အားသာချက်များကို ရရှိကြပြီး ငွေအနှစ်ကို မှီခိုနေရဆဲ ပြိုင်ဘက်များကို ဖိအားပေးသည့် ပြင်းထန်သော ဈေးနှုန်းဗျူဟာများကို ဖွင့်ပေးသည်။.

ထိပ်တန်း ထုတ်လုပ်သူများ၏ အားသာချက်

ထိပ်တန်း ပေါင်းစပ်ထုတ်လုပ်သူများ—ဆဲလ်နှင့် မော်ဂျူးထုတ်လုပ်မှုကို ထိန်းချုပ်သူများသည် de-silvering အကျိုးကျေးဇူးများကို ရယူရန် အကောင်းဆုံးနေရာတွင် ရှိနေသည်။ ကဲ့သို့သော ကုမ္ပဏီများ LONGi, Jinko Solarနှင့် Trina Solar ထိရောက်မှုအကျိုးအမြတ်များကို အမြင့်ဆုံးရရှိစေရန် ဆဲလ်-မော်ဂျူး ပေါင်းစပ်မှုကို အကောင်းဆုံးဖြစ်အောင် လုပ်ဆောင်နေစဉ် ကြီးမားသော ထုတ်လုပ်မှုပမာဏများတွင် လျှပ်စစ်ဖြင့် သတ္တုချလိုင်းများအတွက် လိုအပ်သော အရင်းအနှီးမြှုပ်နှံမှုများကို ဖြန့်ဝေနိုင်သည်။.

သေးငယ်သော ထုတ်လုပ်သူများအတွက် စိန်ခေါ်မှုများ

သေးငယ်သော Tier-2 နှင့် Tier-3 ထုတ်လုပ်သူများသည် ပိုမိုခက်ခဲသော ရွေးချယ်မှုများကို ရင်ဆိုင်နေရသည်။ ကြေးနီလျှပ်စစ်ဖြင့် သတ္တုချခြင်း၏ အရင်းအနှီးပြင်းထန်မှု—တစ်ဂစ်ဂါဝပ်လျှင် ၁၅-၂၅ သန်း—ကုမ္ပဏီများစွာအတွက် တားမြစ်ထားသော အတားအဆီးတစ်ခုကို ကိုယ်စားပြုသည်။ ဤကစားသမားများအတွက်၊, ငွေဖြင့် ဖုံးအုပ်ထားသော ကြေးနီအနှစ် အဓိပ္ပါယ်ရှိသော ကုန်ကျစရိတ် သက်သာမှုကို ပေးစွမ်းနိုင်စဉ် အနည်းဆုံး အရင်းအနှီးမြှုပ်နှံမှု လိုအပ်သောကြောင့် ပိုမိုလွယ်ကူသော လမ်းကြောင်းကို ပေးပါသည်။.

ထောက်ပံ့ရေးကွင်းဆက် အနှောင့်အယှက်

စက်ပစ္စည်းနှင့် ပစ္စည်းထောက်ပံ့ရေးကွင်းဆက်သည်လည်း သိသာထင်ရှားသော အနှောင့်အယှက်များကို ကြုံတွေ့နေရသည်။ လျှပ်စစ်ဖြင့် သတ္တုချခြင်းသည် ဝေစုရရှိလာသည်နှင့်အမျှ စခရင်ပုံနှိပ်စက်ပစ္စည်း ထုတ်လုပ်သူများသည် လျော့နည်းလာသော ဝယ်လိုအားကို ရင်ဆိုင်နေရသည်။ ဆန့်ကျင်ဘက်အားဖြင့်၊ ကဲ့သို့သော အထူးပြု သတ္တုချစက်ပစ္စည်း ပေးသွင်းသူများ Suzhou Maxwell Technologies အချို့က ၀င်ငွေတိုးနှုန်းထက် ကျော်လွန်ကြောင်း အစီရင်ခံတင်ပြခြင်းဖြင့် ကြီးမားသော အမှာစာ နောက်ကျခြင်းများကို လုံခြုံအောင် ပြုလုပ်နေကြသည်။ တစ်နှစ်ထက်တစ်နှစ် ၂၀၀%.

ပထဝီဝင်ဆိုင်ရာ သက်ရောက်မှုများ

ဆိုလာထုတ်လုပ်မှုတွင် တရုတ်နိုင်ငံ၏ လွှမ်းမိုးမှုသည် de-silvering အကူးအပြောင်းကို ဦးဆောင်ရန် နေရာချထားသည်။ ခန့်မှန်းခြေအားဖြင့် ကမ္ဘာလုံးဆိုင်ရာ ဆဲလ်ထုတ်လုပ်မှုစွမ်းရည်၏ ၇၀% and strong government support for technology upgrades, Chinese manufacturers can deploy new metallization technologies at scale more rapidly than competitors in other regions.

Impact on Silver Markets

If copper metallization captures 10% of global cell production by 2027, 30% by 2028, and 50% by 2030, solar silver demand could decline from approximately 200 million ounces in 2025 to 100 million ounces by 2030. This would represent a dramatic reversal of the growth trend that has characterized the past decade.

Silver Recovery and Circular Economy Opportunities

As the installed base of solar panels grows—approaching 2 terawatts of cumulative global capacity by 2026—end-of-life module recycling is emerging as a significant secondary silver source. Each retired panel contains approximately 15-25 grams of silver, representing substantial value at current prices.

Current Recycling Status

Current recycling rates remain low, with estimates suggesting less than 10% of retired panels enter formal recycling channels. The primary barrier is economic: disassembly, separation, and refining processes are labor-intensive and energy-intensive. However, at prices above $50 per ounce, the economics shift dramatically.

Advanced Recycling Technologies

Thermal delamination processes use controlled heating to separate the encapsulant layers, allowing mechanical removal of cells from glass and frames. Chemical leaching then dissolves the silver from cell surfaces, with electrolytic refining producing high-purity silver suitable for reuse in paste manufacturing. Some facilities report silver recovery rates exceeding 95%.

Regulatory Support

ဟိ European Union’s Circular Economy Action Plan mandates improved recovery of precious metals from electronic waste, including solar panels, with specific targets for collection rates and material recovery percentages. တရုတ်နိုင်ငံ has implemented extended producer responsibility (EPR) frameworks requiring manufacturers to fund end-of-life management.

Future Projections

By 2030, cumulative retired panel volume in China alone could reach 18 gigawatts (approximately 1.5 million tons), containing roughly 270-450 tons of recoverable silver. By 2050, global retired capacity may exceed 250 gigawatts, with silver content potentially reaching 3,750-6,250 tons—equivalent to 10-15% of current annual silver mine production.

Future Outlook: Toward a Silver-Independent Solar Industry

The convergence of technological maturity, economic pressure, and strategic necessity is driving the solar industry toward fundamental independence from silver within the next decade. While complete elimination remains unlikely, the mainstream manufacturing base is clearly transitioning to copper-dominant metallization.

Accelerated Timeline

Industry roadmaps published in 2023 anticipated gradual silver reduction through incremental thrifting, with copper electroplating reaching 10-15% market share by 2030. However, the dramatic price surge of 2024-2025 has compressed this timeline significantly. Current deployment announcements suggest copper-based metallization could reach 30-40% of global production by 2027-2028, with potential for majority market share by 2030.

Critical Success Factors

Technical Performance Validation: Technical performance must be validated through long-term field testing, as the solar industry’s ၂၅-၃၀ နှစ် အာမခံစံနှုန်းများကို ထောက်ပံ့ပေးသည်။ require confidence in reliability under diverse environmental conditions. Copper’s susceptibility to oxidation and corrosion remains a concern that will only be resolved through extended outdoor exposure data.

Capital Availability: The substantial investment required for electroplating lines creates barriers for smaller manufacturers and may slow transition in markets with limited access to low-cost capital. However, the compelling economics of copper metallization at current silver prices suggest that manufacturers unable to transition may face existential threats.

Policy and Regulatory Factors: Some markets may require extended field validation or certification processes before approving copper-metallized modules for utility-scale installations or subsidy programs. Conversely, government support for domestic manufacturing capacity could accelerate copper electroplating deployment by subsidizing capital investments.

Broader Implications

Silver’s role as a critical material for clean energy transitions has been a central narrative supporting investment demand and price appreciation. If solar consumption peaks and declines as projected, silver’s strategic importance may diminish, potentially affecting long-term price trajectories. However, growing demand from electric vehicles, လွ်ပ္စစ္ပစၥည္းမ်ား, and emerging applications like antimicrobial coatings may sustain overall industrial consumption.

Industry Transformation

For solar manufacturers, the de-silvering transition represents both challenge and opportunity. Those that successfully navigate the technological and capital requirements will emerge with sustainable cost structures independent of precious metal volatility, positioning them for long-term competitiveness. Those that fail to adapt risk margin compression and potential obsolescence. နောက်ငါးနှစ်အတွင်း ဆိုလာငွေခေတ်လွန်ကာလတွင် မည်သည့်ထုတ်လုပ်သူများ ဆက်လက်ရှင်သန်ကြီးထွားမည်ကို ဆုံးဖြတ်ဖွယ်ရှိသည်။.

နှိုင်းယှဉ်ဇယား- ဆိုလာဆဲလ်နည်းပညာအလိုက် ငွေပါဝင်မှု

| ဆဲလ်နည်းပညာ | ငွေပါဝင်မှု (mg/cell) | ငွေပါဝင်မှု (mg/W) | ပုံမှန်စွမ်းဆောင်ရည် | ငွေဖယ်ရှားနိုင်မှု | ၂၀၂၅ ခုနှစ် ဈေးကွက်ဝေစု |

|---|---|---|---|---|---|

| P-type PERC | 100-110 | 18-20 | 22-23% | အသင့်အတင့် (Cu @Ag paste) | 35% |

| N-type TOPCon | 80-90 | 15-17 | 24-25% | ကောင်း (Cu @Ag paste, dual-layer) | 45% |

| Heterojunction (HJT) | 70-75 | 12-14 | 25-26% | အလွန်ကောင်း (Cu @Ag paste, Cu plating) | 12% |

| Back-Contact (BC) | 130-135 | 20-22 | 26-27% | အလွန်ကောင်း (Cu plating) | 5% |

| Cu-Plated HJT | 0-15 | 0-3 | 25-26% | ပြည့်စုံ (ငွေမပါ) | 2% |

| Cu-Plated BC | 0-10 | 0-2 | 26-27% | ပြည့်စုံ (ငွေမပါ) | 1% |

မှတ်ချက်- ငွေပါဝင်မှုသည် ထုတ်လုပ်သူနှင့် သီးခြားဆဲလ်ဒီဇိုင်းပေါ်မူတည်၍ ကွဲပြားနိုင်သည်။ ပုံများသည် ၂၀၂၅ ခုနှစ် ထုတ်လုပ်မှုအတွက် စက်မှုလုပ်ငန်းပျမ်းမျှကို ကိုယ်စားပြုသည်။.

ငွေဖယ်ရှားခြင်းနည်းပညာ နှိုင်းယှဉ်ချက်

| နည္းပညာ | ငွေလျှော့ချခြင်း | ရင်းနှီးမြှုပ်နှံမှု | အကောင်အထည်ဖော်ချိန် | နည်းပညာရင့်ကျက်မှု | မူလဆဲလ်နှင့် လိုက်ဖက်ညီမှု |

|---|---|---|---|---|---|

| ငွေဖြင့်အုပ်ထားသော ကြေးနီအနှစ် (Cu @Ag) | 50-80% | နည်း ($1-3M/GW) | ၆-၁၂ လ | ဂုိေဒါင္ | ဆဲလ်အမျိုးအစားအားလုံး |

| နှစ်ထပ်အနှစ် (Seed + Cu @Ag) | 50-70% | နည်း ($2-4M/GW) | ၁၂-၁၈ လ | ဂုိေဒါင္ | TOPCon, PERC |

| ကြေးနီလျှပ်စစ်ဖြင့် သတ္တုရည်စိမ်ခြင်း | 95-100% | မြင့် ($15-25M/GW) | ၂၄-၃၆ လ | စောစီးစွာ စီးပွားဖြစ် | HJT, BC |

| အကောင်းဆုံး Grid ဒီဇိုင်း (MBB/Zero-BB) | 10-20% | အသင့်အတင့် ($3-6M/GW) | ၁၂-၁၈ လ | ဂုိေဒါင္ | ဆဲလ်အမျိုးအစားအားလုံး |

| နာနိုငွေအနှစ် | 15-25% | နည်း ($1-2M/GW) | ၆-၁၂ လ | ဂုိေဒါင္ | ဆဲလ်အမျိုးအစားအားလုံး |

ရင်းနှီးမြှုပ်နှံမှုဆိုင်ရာ ပုံများသည် လက်ရှိထုတ်လုပ်မှုလိုင်းများ ပြန်လည်တပ်ဆင်ခြင်း သို့မဟုတ် အစိမ်းရောင်မြေနေရာချထားခြင်းအတွက် တိုးမြှင့်ကုန်ကျစရိတ်များကို ကိုယ်စားပြုသည်။.

FAQ Section

မေး- ဆိုလာထုတ်လုပ်သူများသည် ကြေးနီသို့ ချက်ချင်းမပြောင်းနိုင်ရသည့် အကြောင်းရင်းမှာ အဘယ်နည်း။

ဖြေ- ကြေးနီတွင် အရေးပါသော နည်းပညာဆိုင်ရာ အတားအဆီးနှစ်ခုရှိသည်။ အပူချိန်မြင့်မားစွာတွင် ဓာတ်တိုးခြင်း နှင့် “ဆီလီကွန်၏ ”ကြေးနီအဆိပ်သင့်ခြင်း". ရိုးရာဆဲလ်ထုတ်လုပ်မှုအတွက် လိုအပ်သော 700-900°C မီးဖုတ်အပူချိန်နှင့် ထိတွေ့သောအခါ ကြေးနီသည် လျင်မြန်စွာ ကြေးနီအောက်ဆိုဒ်အဖြစ်သို့ ပြောင်းလဲသွားပြီး လျှပ်ကူးနိုင်စွမ်းအားနည်းသည်။ ထို့အပြင် ကြေးနီအက်တမ်များသည် အပူချိန်မြင့်မားစွာတွင် ဆီလီကွန်ထဲသို့ ပျံ့နှံ့သွားပြီး ဆဲလ်စွမ်းဆောင်ရည်ကို 20-50% အထိ လျှော့ချပေးသည့် ချို့ယွင်းချက်များကို ဖန်တီးပေးသည်။ အဆင့်မြင့်ဆဲလ်ပုံစံများကဲ့သို့ HJT နှင့် back-contact ဒီဇိုင်းများ အပူချိန်နိမ့်သော ထုတ်လုပ်မှုနှင့် ပျံ့နှံ့မှုအတားအဆီးအလွှာများမှတစ်ဆင့် ဤပြဿနာများကို ဖြေရှင်းပေးသော်လည်း ဤနည်းပညာများသည် လုံးဝအသစ်သော ထုတ်လုပ်ရေးကိရိယာများ လိုအပ်ပြီး လက်ရှိကမ္ဘာ့စွမ်းဆောင်ရည်၏ 15-20% သာရှိသည်။.

မေး- ငွေဈေးနှုန်းမြင့်တက်ခြင်းသည် ဆိုလာပြားကုန်ကျစရိတ်ကို မည်မျှအထိ သက်ရောက်မှုရှိသနည်း။

ဖြေ- လက်ရှိစားသုံးမှုအဆင့် (ပြားတစ်ချပ်လျှင် ခန့်မှန်းခြေ ၂၀ ဂရမ်) တွင်၊ $10 per ounce increase ငွေဈေးနှုန်းများ မြင့်တက်လာခြင်းသည် ခန့်မှန်းခြေအားဖြင့် $6-7 ပုံမှန် 400-ဝပ် လူနေအိမ်သုံးပြားတစ်ချပ်၏ ကုန်ကျစရိတ်သို့ ထပ်ပေါင်းထည့်သည်။ ၂၀၂၄-၂၀၂၅ ခုနှစ်အတွင်း ငွေဈေးနှုန်းများသည် တစ်အောင်စလျှင် $25 မှ $80+ သို့ မြင့်တက်လာခြင်းနှင့်အတူ ဤသည်မှာ ခန့်မှန်းခြေအားဖြင့် ပြားတစ်ချပ်လျှင် $35-40 ကုန်ကျစရိတ်ပိုများလာခြင်းကို ကိုယ်စားပြုသည်။, သို့မဟုတ် တစ်ဝပ်လျှင် $0.09-0.10. တစ်ဝပ်လျှင် $0.15-0.20 ဝန်းကျင်ဖြင့် ဈေးနှုန်းသတ်မှတ်ထားသော အသုံးအဆောင်လုပ်ငန်းသုံး ပရောဂျက်များအတွက် ဤသည်မှာ 45-65% တိုးလာခြင်း ကုန်ကြမ်းကုန်ကျစရိတ်တွင် ထုတ်လုပ်သူအမြတ်အစွန်းကို ပြင်းထန်စွာ ဖိအားပေးသည်။.

မေး- အဟောင်းပြားများမှ ပြန်လည်အသုံးပြုထားသော ငွေသည် ထောက်ပံ့မှုပြဿနာကို ဖြေရှင်းနိုင်မည်လား။

ဖြေ- မကြာမီကာလအတွင်း မဖြေရှင်းနိုင်ပါ။ သက်တမ်းကုန်ဆုံးသွားသော ပြားတစ်ချပ်စီတွင် ပြန်လည်ရယူနိုင်သော ငွေ ၁၅-၂၅ ဂရမ်ပါဝင်သော်လည်း သက်တမ်းကုန်ဆုံးသွားသော ပြားအရေအတွက်သည် အတော်လေးနည်းပါးနေသေးသည်—ခန့်မှန်းခြေအားဖြင့် ၂၀၃၀ ပြည့်နှစ်တွင် ကမ္ဘာတစ်ဝန်း တန်ချိန် ၁-၂ သန်း, ဖြစ်ပြီး၊ ခန့်မှန်းခြေအားဖြင့် ငွေ တန်ချိန် ၃၀၀-၅၀၀. ပါဝင်သည်။ ဤသည်မှာ ခန့်မှန်းခြေအားဖြင့် ကမ္ဘာ့ငွေထောက်ပံ့မှု၏ ၁-၂၁TP3T. သာရှိသည်။ ၂၀၅၀ ပြည့်နှစ်တွင် စုစုပေါင်း သက်တမ်းကုန်ဆုံးသွားသော စွမ်းဆောင်ရည်သည် ၂၀၀+ ဂစ်ဂါဝပ်သို့ ရောက်ရှိသောအခါ ပြန်လည်အသုံးပြုထားသော ငွေသည် ထောက်ပံ့ပေးနိုင်မည်ဖြစ်သည်။ 3,000-5,000 tons annually (approximately 10-15% of current mine production), but this timeline extends well beyond the current supply crisis.

Q: What happens to silver prices if solar demand decreases?

A: Solar currently represents approximately 17-20% of total silver demand and nearly 30% of industrial demand. If copper metallization reduces solar silver consumption by 50% over 5 years, this would remove approximately 100 million ounces from annual demand—roughly 10% of total global consumption. However, growing demand from electric vehicles (projected to triple by 2030), လွ်ပ္စစ္ပစၥည္းမ်ားနှင့် medical applications may partially offset this decline. Most analysts expect silver prices to moderate from 2025 peaks but remain elevated relative to pre-2024 levels due to persistent industrial demand and ongoing supply constraints.

Q: Which solar cell technology will dominate by 2030?

A: Industry consensus suggests TOPCon will maintain plurality market share (40-50%) through 2030 due to its balance of efficiency, cost, and manufacturing compatibility with existing equipment. However, heterojunction (HJT) နှင့် back-contact technologies are projected to grow from current 15-20% combined share to 30-40% by 2030, driven primarily by their superior compatibility with copper metallization and higher efficiency potential. The key variable is whether copper electroplating achieves projected cost parity with silver-based TOPCon; if so, HJT/BC growth could accelerate beyond current projections.

Q: Are there any alternatives to both silver and copper?

A: Researchers are exploring several options, including aluminum, nickelနှင့် conductive polymers, but none currently match silver or copper’s combination of conductivity, processability, and cost. Aluminum has been used for rear-side contacts but suffers from high contact resistance and poor solderability for front-side applications. Nickel requires complex plating processes and has lower conductivity than copper. Conductive polymers remain in early research stages with conductivity orders of magnitude below metals. For the foreseeable future, the choice remains between silver-based pastes, silver-copper compositesနှင့် pure copper metallization.

Related Links

- အကြောင်းအရာများအကြောင်းပိုမိုလေ့လာရန် solar combiner box design and protection

- Understand DC circuit breaker requirements for photovoltaic systems

- Explore junction box specifications for solar panel connections

- Discover surge protection strategies for solar installations

- Review electrical panel components for renewable energy systems

VIOX Electric အကြောင်း: As a leading B2B manufacturer of electrical equipment, VIOX Electric provides comprehensive solutions for solar energy systems, including DC circuit breakers, surge protection devices, combiner boxes, and distribution panels. Our products meet international standards (IEC, UL, CE) and support the global transition to renewable energy with reliable, cost-effective electrical protection and control equipment.